Individual Pension Plans (IPP) in Canada

IPPs are ideal for business owners who want a secure, tax-efficient way to build long-term wealth.

Individual Pension Plans (IPP) are a CRA-approved defined benefit retirement plan for incorporated Canadians. They offer higher contribution limits than RRSPs, allow corporate tax deductions, provide creditor protection, and deliver predictable retirement income.

What Is an Individual Pension Plan (IPP)?

An Individual Pension Plan (IPP) is a CRA-compliant registered retirement plan that helps incorporated professionals convert corporate earnings into secure, tax-efficient retirement income through a structured pension.

An IPP makes it possible to:

- Build more retirement wealth with contribution limits that surpass RRSPs

- Use corporate dollars, instead of personal income, to fund your pension plan

- Reduce taxes because contributions, fees, and investment management costs are deductible to the corporation

- Catch up fast with past service funding if earlier retirement saving years were missed or inconsistent

- Support your family’s future by adding adult children employed in the business and transferring assets to them on a tax-deferred basis

- Safeguard your savings through creditor and lawsuit protection

Most importantly, an IPP allows you to retire with a predictable pension income, even when investment markets swing.

Who Should Consider an Individual Pension Plan in Canada?

An IPP is ideal if you:

- Earn at least $80,000+ in T4 salary

- Are 40+ and frustrated with RRSP limits

- Want to reduce corporate taxes

- Have retained earnings sitting in your corporation

- Want a predictable retirement income

- Are worried about protecting assets from creditors

- Prefer a done-for-you, compliant strategy you don’t have to manage

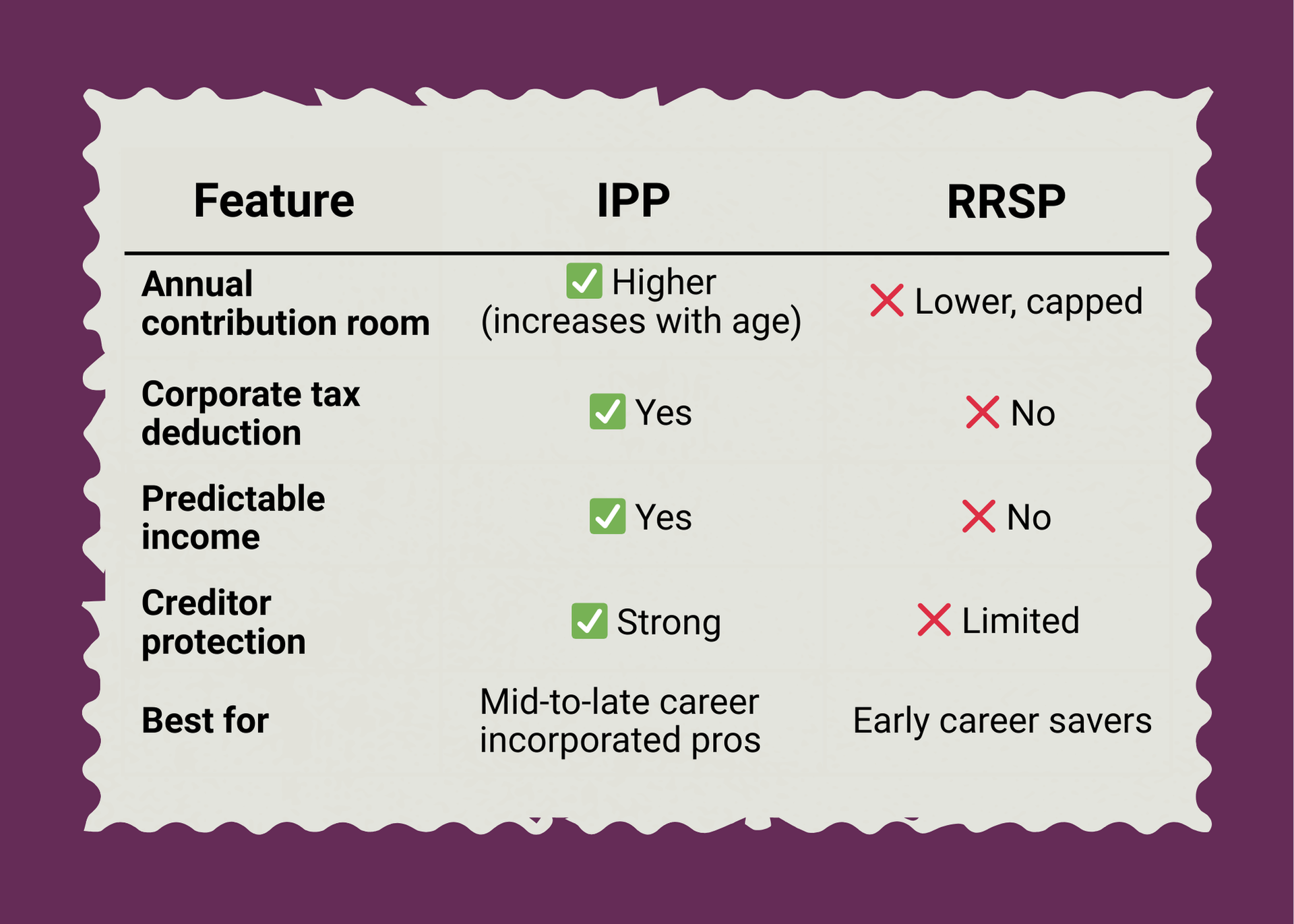

IPP vs RRSP (Quick Comparison)

The

IPP vs RRSP decision comes down to how much control, contribution room, and tax efficiency you want. Here's a quick comparison to highlight the key differences and help you find the best fit:

- Actuarial plan setup and CRA registration

- Annual valuations and compliance reporting

- Investment coordination and pension projections

- Retirement income planning, terminal funding, and past service calculations

- Support for multi-member and family IPPs

- Ongoing strategic advice for tax efficiency and long-term planning

Why Smart Business Owners in Canada Choose IPPs?

01

Escape the RRSP Ceiling

RRSP limits can feel like a cap on your future. IPP contributions increase with age, allowing significantly more than RRSPs.

More room means more retirement wealth, faster.

02

Reduce Personal & Corporate Tax Burden

If you're tired of writing large cheques to CRA every year, an IPP is one of the most powerful, legal tax-reduction tools available.

Your corporation can deduct:

- Annual contributions

- Past service contributions

- Administration and actuarial fees

03

Move Wealth Out of the Corporation Without Punishing Tax

Many owners feel frustrated with retained earnings trapped inside the business.

IPP contributions let you transfer corporate dollars into personal retirement wealth tax-efficiently. This is especially valuable before a sale, succession, slowdown, or planned exit.

04

Predictable Income Removes the Guesswork From Retirement

If market swings make you anxious, or you simply want to know you’ll have enough, an IPP provides:

- Defined, guaranteed retirement income

- Optional inflation protection

- Survivor benefits

With an IPP, your retirement plan becomes something you can count on instead of a best-guess projection.

05

Risk Protection

RRSPs can be vulnerable. Business ownership comes with uncertainty.

IPP assets are creditor-protected, even during legal, financial, or industry challenges.

If the unexpected happens, your retirement stays safe.

06

Worried About Selling Your Business? An IPP Reduces the Pressure

Business value is never guaranteed, and an IPP ensures your retirement isn’t tied to selling your business at the perfect time or price. It gives you freedom and flexibility, even if you exit earlier than planned or during a down market.

07

Catch Up Room

If inconsistent RRSP years, career breaks, or reinvesting in your business affected your contributions, an IPP helps you accelerate savings through:

- Past service funding (catch-up contributions)

- Terminal funding (major boost at retirement)

How Our IPP Process Works

Want to See How Much More

You Could Contribute With an IPP?

We’ll calculate your contribution limits, tax deductions, and retirement income at no cost. Book your free consultation today.

Contact Us

FAQs

About IPPs: Contributions, CRA Rules & Retirement Benefits

1. How does an Individual Pension Plan work under CRA rules?

An IPP must be registered with the CRA, follow defined benefit funding formulas, and file actuarial valuations and required reports. Benefits are paid under the plan terms at retirement.

2. What are the contribution limits for an Individual Pension Plan in Canada?

IPP contributions are actuarially determined using CRA-prescribed defined benefit formulas that depend on age, T4 salary, and pensionable service. They are not a flat cap like RRSPs. Older members generally have higher allowable contributions.

3. How do retirement benefits from an IPP compare to an RRSP?

An IPP provides defined, formula-based pension benefits payable under plan terms, subject to CRA rules (including the IPP minimum amount after age 71). An RRSP offers no guaranteed payout, and withdrawals depend on investments and conversion choices.

4. Can I estimate my IPP contributions with a calculator?

You can approximate using age, salary, and service, but only an actuary can certify the actual IPP contributions (including past-service and any funding adjustments) under CRA formulas.

5. Are IPP assets creditor-protected?

Yes, in most provinces, IPP assets are protected under pension legislation, which means they’re generally shielded from creditors if your business faces a lawsuit, financial trouble, or even bankruptcy.

6. Can I manage my own IPP investments?

No, an IPP must be set up and managed by a licensed professional who follows pension investment rules. While you can provide input on your goals and risk tolerance, the oversight is handled for you. This protects the plan, ensures compliance with strict standards, and removes the workload and risk of managing the investments yourself.